Research & Ideation

현장에서 시작한 문제 정의 Problem definition from the field

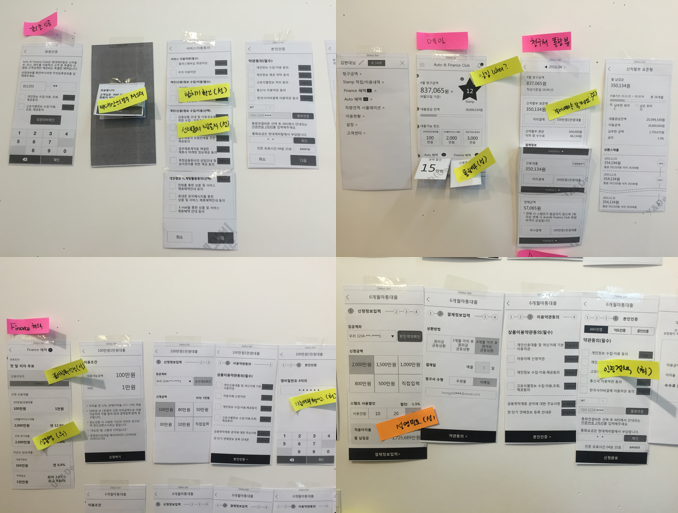

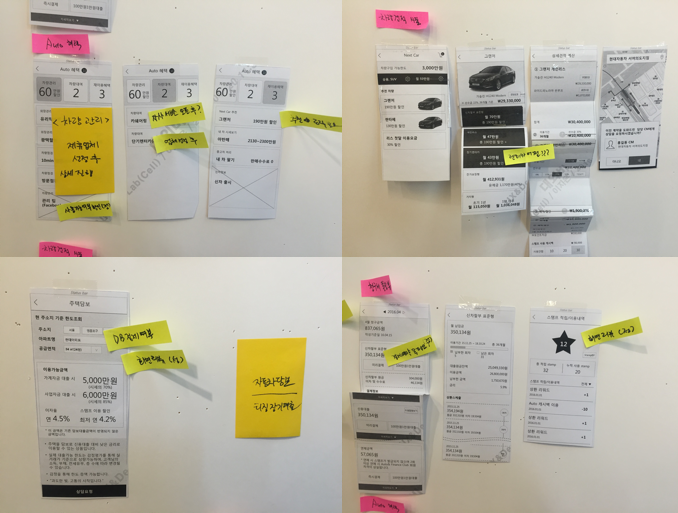

사용자 인터뷰와 현장 관찰에서 반복적으로 발견된 패턴이 있었습니다. 고객은 "좋은 상품을 찾는" 것이 아니라, "내가 받을 수 있는 것"을 파악하는 데 에너지를 쏟고 있었습니다. 이 차이가 설계 방향을 바꾸었습니다.

A consistent pattern emerged from user interviews and field observation. Customers weren't trying to find a "good product" — they were spending energy just figuring out what they could actually get. That distinction changed everything about the design direction.

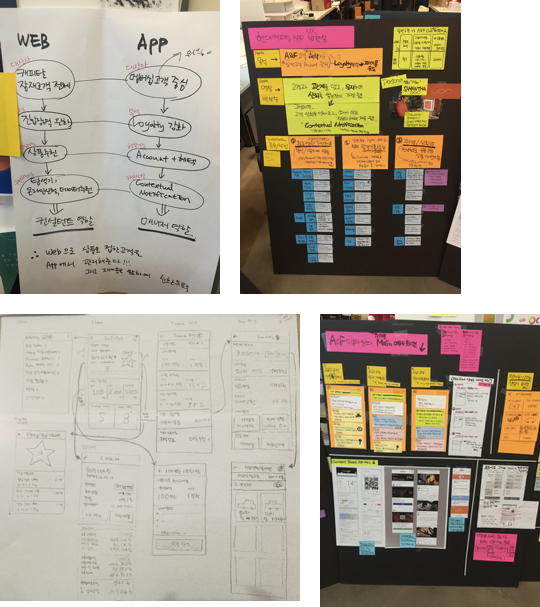

팀은 여정 맵, 콘텍스추얼 인콰이어리, 내부 데이터 분석을 병행했습니다. "고객이 실패하는 지점"과 "고객이 이탈하는 지점"이 다르다는 것을 데이터로 확인했고, 이를 설계 기준으로 삼았습니다. The team combined journey mapping, contextual inquiry, and internal data analysis. We confirmed through data that "where customers fail" and "where customers drop off" are different — and used that as the design foundation.